Student loan payments are no longer something borrowers can leave on the side and hope to fix later. A major repayment shift is now in motion, and the most important date to watch is July 1, 2026.

That is when federal loan servicers will start sending notices to borrowers who were enrolled in the SAVE Plan, telling them to move into another legal repayment plan within a set 90-day window. The U.S. Department of Education says borrowers who do not make a choice in time may be moved into the Standard Repayment Plan or the new Tiered Standard Plan.

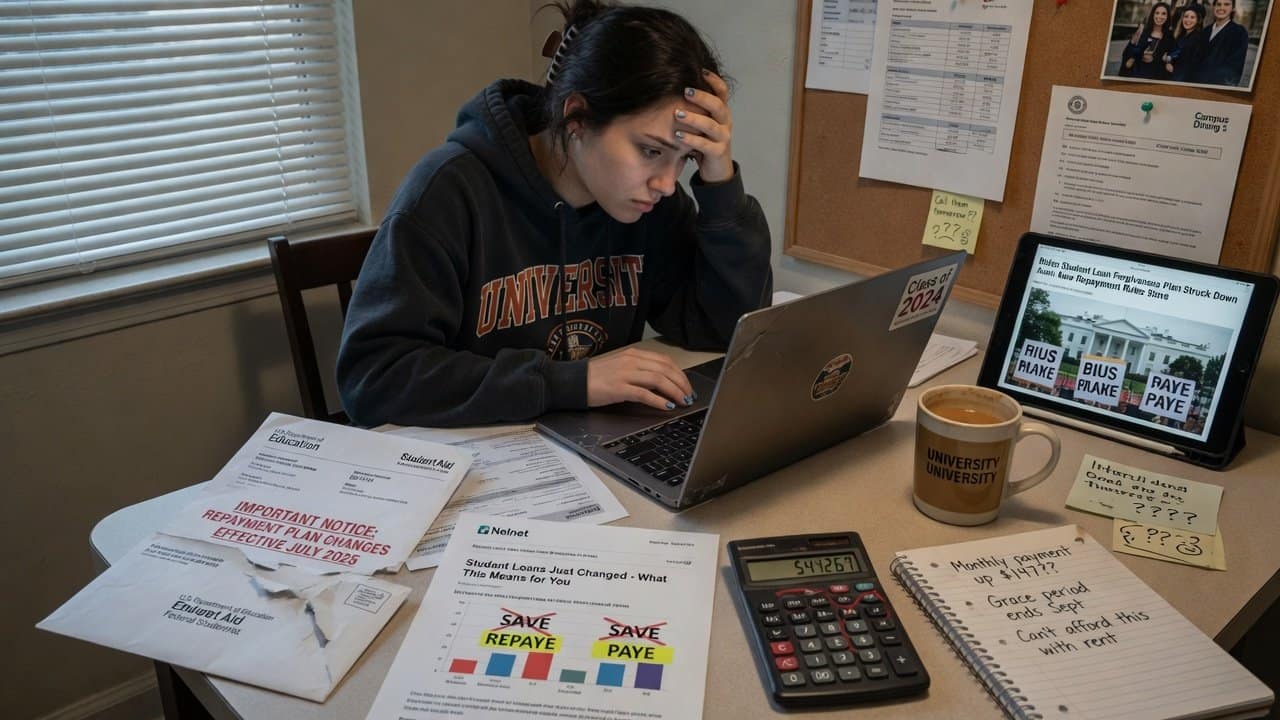

The SAVE Plan Is Ending For Borrowers

The Department of Education has said the SAVE Plan has ended, and more than 7.5 million borrowers enrolled in it will need to choose another repayment option. This matters because many people on SAVE had lower monthly payments, and some may now face a different bill once they move to a new plan.

The exact deadline will not be the same for everyone. Servicers will send each borrower their own 90-day deadline after notices begin on July 1.

Borrowers do not have to wait for that notice to start preparing. The Department says a borrower may contact their servicer at any time to move into a legal repayment plan.

That is important because waiting until the last few days can leave less room to compare options, fix missing paperwork, or update income details.

A New Repayment Plan Is Coming

A new option called the Repayment Assistance Plan, or RAP, is scheduled to launch on July 1, 2026. According to the Department, RAP will base monthly payments on a borrower’s income and number of dependents.

The Department also says borrowers who make full, on-time payments under RAP will be protected from runaway interest and will keep making progress on the loan’s principal balance.

The new Tiered Standard Plan will also begin on July 1. It will use fixed repayment terms of 10, 15, 20, or 25 years, based on the borrower’s total loan balance.

This could matter most for borrowers with larger balances, since a longer term may lower the monthly bill but can also keep the debt around for more years.

IDR Applications Are Still Open

Borrowers who need a payment tied to income can still look at income-driven repayment options. Federal Student Aid says the online IDR application is available, and applying is free.

On IDR plans, monthly payments are based on income and family size. Current listed IDR options include Income-Based Repayment, Income-Contingent Repayment, and Pay As You Earn.

A small step can also speed things up. The Department says IDR applications can be processed faster when borrowers allow the Department to get federal tax information directly from the IRS. That can reduce the need to upload income documents by hand.

New Loan Limits May Affect Families

The changes are not only about repayment. New borrowing limits are also being added for the 2026–27 award year. Federal Student Aid says Parent PLUS loans will have a $65,000 aggregate limit per dependent student.

Once that limit is reached, parent borrowers will not be eligible to borrow more PLUS loans for that student, even if earlier loans are repaid, forgiven, or discharged.

Student borrowers will also have a new lifetime maximum aggregate loan limit of $257,500. That total includes undergraduate, graduate, and professional loans under Direct Loans and FFEL loans. Graduate and professional PLUS loans count toward that lifetime limit, but Parent PLUS loans do not.

What Borrowers Should Do Now

The safest move is to check the loan servicer account, confirm the current repayment plan, and make sure contact details are correct. Borrowers leaving SAVE should compare the Standard Plan, Tiered Standard Plan, RAP, and available IDR options before the 90-day window closes.

Parents and future graduate students should also look at the new borrowing caps before making school payment plans.

The key point is simple: student loan choices made this summer may shape monthly bills for years. Waiting may feel easier today, but it can leave borrowers with fewer choices later.